"The trouble with people is not that they don't know but that they know so much that ain't so."

The above quote is absolutely lovely; there's something similar in Taleb's The Black Swan; my beloved McCloskey has a similar quote in the first book about the Bourgeois era Bourgeois Virtue, I think; I thought Mark Twain was credited with something similar, but wikiquote says this one comes from Josh Billings. It's kinda great, and very much how I approach my friends on the left. I'm so humble.

During my readings for an essay on the Australian Superannuation system (their compulsory private pension system, usually called 'super') I stumbled upon quite exciting data. Whenever I'm doing the reading for my essays I tend to find great stuff, which obviously make the essay-writing process slightly lengthier. This stuff comes from all the amazing data in the HILDA survey (Household Income Labour Dynamics Australia), more specifically from Richard Finlay's article about the 2010 data and the summary of the 2015 data. The HILDA survey is published by the University of Melbourne Melbourne Institute, and is perhaps the most extensive survey data gathering on household's financial situation. By no means perfect, it is quite useful (especially when comparing to national accounts) in order to draw conclusions on the Australian population.

So let's have a look at a couple of common ideas that the HILDA report kinda ruthlessly destroys:

1) Inequality is increasing

Since the sky is falling and the rich are getting richer and the poor are falling behind and neoliberalism has failed and whatnot, you'd expect maybe that basic claim of inequality of income to be true...? We already knew the Gini-coefficient of income inequality for the U.K. was the same last year as 25 years ago, but surprisingly enough, Australia joins the ranks where inequality has remained pretty stable:

As seen, the inequality of incomes for Australian households, measured in Gini, P90/P50 or P50/P10 yields rather stable, if not slightly falling values. The last 15 years do not bear out the claim about increasing inequality. Same goes for 5-year moving averages:

2) The Housing Market has gone Bananas

Well, maybe. This claim is slightly less silly than the previous, but the data nevertheless shows a couple of awkward things if your favourite Chicken-Little pet-project is housing markets rather than inequality.

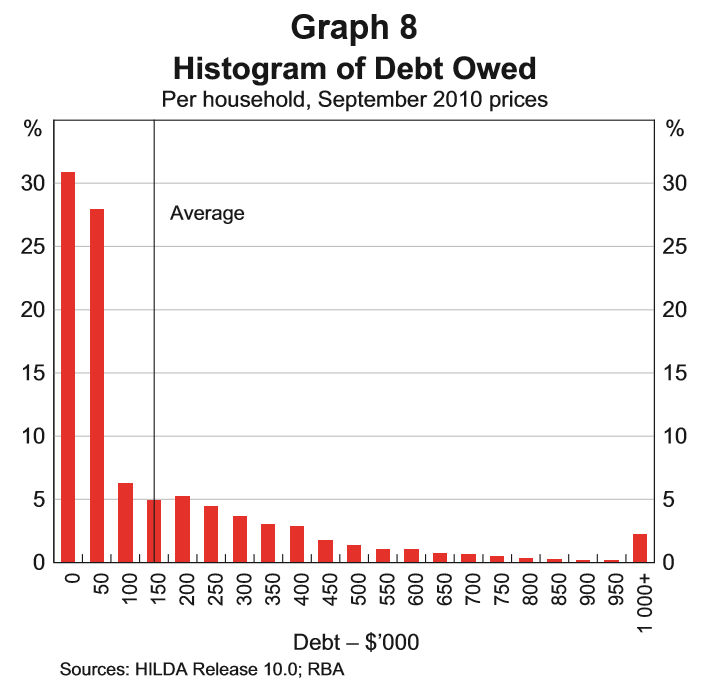

Finlay reports that around half (p. 24) of home-owners own their house outright - that is, with the mortgage paid off. Furthermore, this graph should make most permabears* (Hi, Tepper!) think twice [*= a permabear is someone who constantly believes the markets are about to crash, a Chicken Little yelling about the massive risks of <insert whatever>]:

In the above chart 31% of households have hold no debt - I mean no debt. And another 28% owe largely trivial amounts (<50k). Now, that data is about 6 years old, and things can be very different today, but more recent RBA statistics indicate no such thing; yes, some of the ratios are visibly higher, but they don't change the overall pattern as outlined from the 2010 HILDA:

a) most debt is overwhelmingly concentrated in the high-income quintiles, i.e. those best able to carry and service that debt;

b) debt-to-asset ratios are remarkably low across the board (25-30%), and has been falling since around 2012; this indicate that housing prices could fall by something like half, and most households would stay solvent and able to service their debts;

c) Since the ratio of interest payments to disposable income (something like 8%) is the lowest since 2003, the permabear worry about crash leading to widespread insolvency is overstated. At most, in such a scenario some retail shops might have to close - hardly the end of the world.

Staring oneself blind on aggregate data won't tell you very much. You have to look deeper - at which point you find that the risks indignantly raised by permabears is much smaller than they claim.

Staring oneself blind on aggregate data won't tell you very much. You have to look deeper - at which point you find that the risks indignantly raised by permabears is much smaller than they claim.

McCloskey had an amazing quote in an interview at GMU the other day, which also sadly applies very well to me:

I say to my libertarian friends that 'Marx was the greatest social scientist of the 19th century', and they all get mad at me. So I turn to my friends on the left and say '... and most of what he said was wrong', and they get mad at me. Which I why I don't have any friends.Pretty much so. No, my lovely permabears, debt-to-income ratios are not a source of concern, and the housing market doesn't have to crash simply because it has recently boomed. You have to look deeper than that.

And no, my lovely friends on the left, inequality has not gotten worse, the rich may be richer, but so are the poor - and there doesn't seem to be any real change in social mobility, neither in Australia not the U.S.

Some Knowledge Just Ain't So.

No comments:

Post a Comment